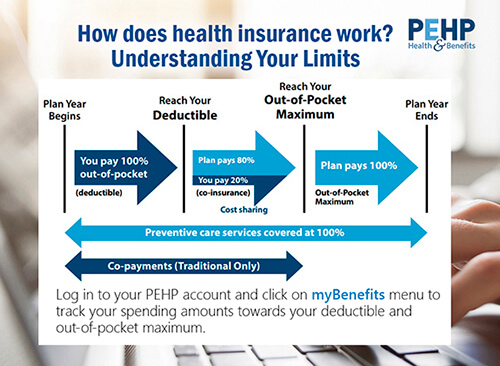

Health Insurance Basics

- Premium – The amount you pay for your health insurance each paycheck. Remember, this is deducted from your paycheck whether you go to the doctor or not. Want a lower or no premium medical plan? Consider enrolling in a high-deductible health plan, such as the STAR HSA Plan.

- Deductible - The amount you must first pay before PEHP begins to pay its coinsurance portion of your claims.

- Copay – Set dollar amount you pay for a service. This amount is applied to the out-of-pocket maximum but is not applied to the deductible. Copays are only available on Traditional Plans.

- Coinsurance - A percentage of the cost you pay for most medical services once the deductible is met and until you’ve reached the out-of-pocket maximum.

- Out-of-Pocket Maximum (OOPM) - The maximum amount your household pays for covered services in a plan year after which PEHP pays 100% for covered benefits at an in-network provider. For plans with an out-of-network benefit, PEHP pays 80% of the in-network rate for covered services at an out-of-network provider.

When you seek care, your provider will send a bill to PEHP for payment of services. We send you an Explanation of Benefits (EOB) each time we process a claim for you or someone on your plan. The EOB is not a bill – it’s a summary of how your benefits apply to the service(s) you received.

In a nutshell, this is what the EOB tells you:

Billed Amount: The amount the provider charges for the service.

Allowed Amount: The contracted rate PEHP has with in-network providers.

Plan Paid: The amount PEHP is responsible to pay based on your cost sharing (coinsurance) plan. For example, your plan may pay 80% of the bill (after you meet your deductible) and you may pay 20%.

Your Responsibility: The amount you are responsible to pay the provider after PEHP has paid its portion.

To see your EOBs online, log in to your PEHP account and click on Claims History under the My Benefits menu. If you believe there is an error in your EOB, please contact us immediately via the Message Center in your PEHP account or call us at 801-366-7555.

Open Enrollment is the only time during the year that you can change your PEHP benefits and get additional coverage for you and your family for the upcoming plan year. Check with your employer to see when Open Enrollment is available to you. The only other time you can add or remove coverage during the year is if you have a MIDYEAR EVENT, such as a new baby, adoption, marriage, divorce, or loss of other insurance coverage.